Hard Money vs. Traditional financing

What is the difference between hard money and traditional financing, and how can you use them both to your advantage? Hard money loans are much shorter and tend to have higher rates than conventional loans. The relatively higher rates are due to the incredibly shorter loan terms and to offset some of the fixed lending costs. Hard money lenders have a much simpler underwriting process, as they only use the asset value to determine if they will lend on a property. This differs significantly from a conventional lender that uses both the asset’s value and the borrower’s creditworthiness.

The asset-only underwiring process allows lenders to close on properties quickly (in as soon as 24hrs at Capital Fund) and lend on distressed properties, where many traditional banks fall short. However, lending on distressed properties and construction also tends to be riskier, and the higher rates are used to mitigate some of that risk.

Buying the property

So, why would you use a higher rate loan? There are many reasons why a borrower might opt for a hard money loan rather than going down the traditional route, such as problems with personal credit or the long process that conventional banks use to approve a loan. Despite the lower rates, traditional lenders require a nauseating amount of information to get approved. From months of bank statements to years of tax returns, and extensive credit history. The whole process may take be as long as 60-90 days before an investor gets to the closing table.

In any business, the cliché time is money rings true, but that is especially poignant in real estate. Today’s housing market is a seller’s market, where offers are plenty and supply is rare. Investors need to piece together offer packages that are not only priced competitively but also have the quickest closing time. Turning in an offer with a 60-90 day close so you can hear back from a big box lender may cost you the whole deal. In these situations, investors turn to private hard money to close deals quickly (in as soon as 24hrs) and have a much more streamlined process than traditional lenders. Some investors may even offset a hard money loan’s carrying cost by offering a competitive price sweetened by a quick close.

cliché time is money rings true, but that is especially poignant in real estate. Today’s housing market is a seller’s market, where offers are plenty and supply is rare. Investors need to piece together offer packages that are not only priced competitively but also have the quickest closing time. Turning in an offer with a 60-90 day close so you can hear back from a big box lender may cost you the whole deal. In these situations, investors turn to private hard money to close deals quickly (in as soon as 24hrs) and have a much more streamlined process than traditional lenders. Some investors may even offset a hard money loan’s carrying cost by offering a competitive price sweetened by a quick close.

Don’t Forget About Rehab

Using hard money to finance the acquisition of the property is a great strategy to leverage your cash during the sale process, but to also allow for rehab funds. Real estate investors have to budget beyond the initial down payment and have to also include items like closing costs, loan carrying costs, and more.

Having more cash available in your bank account will allow you to get started on the rehab right away, which is important so that your investment property can hit the market again as soon as possible. If funds are tight, Capital Fund can even finance 100% of the rehab cost. Some more experienced investors understand the power of leveraging their cash or resources even further. For example, an investor could get reimbursed for rehab costs during the final stages of home improvements. Doing so may provide the necessary capital to tackle an additional property while the others take some time to close with a consumer buyer. Having this extra cash in your bank account is a necessary step when applying to refinance through a long-term lender since they will pull bank statements and credit for loan approval.

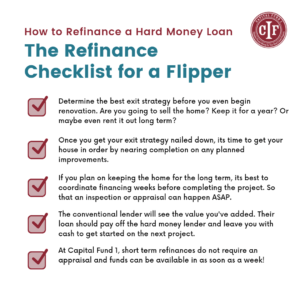

Cash-out, Start over

If you are planning on using the property as a rental, then the next step is to refinance. There are two options of refinancing, you can either refinance with a private lender or into a long-term 30- or 15-year mortgage. The bank will be much more accepting to lend on this property now that it has been renovated and even get higher loan amounts now that value was added to the home. Investors may pull equity from the property with a refinance in both the hard money and conventional scenarios. The cash that you get from the refinance will put you in a much better position to start a new project now that you have a cash-flowing asset and the equity from your past project to go and find a new deal.